You go home for Holi.

Between the colours, gujiyas and family gossip, you start noticing small things.

Your mother moves a little slower in the kitchen.

Your father doesn’t stand as straight as he used to.

In between jokes about your career and wedding plans, your brain goes somewhere else:

- How is their health really?

- What do their days look like when you’re not there?

- And quietly, the big one: Will their money last?

Most middle‑class Indian parents today do have some corpus:

- PF and gratuity

- A few mutual funds

- FDs “for safety”

- Maybe a flat on rent

But having enough and making it last are two very different problems.

How the money comes out matters just as much as how it went in.

Today’s article is about that part—how your parents withdraw from their mutual funds in retirement, and why a wrong choice between IDCW and SWP can quietly increase their tax bill and erode the corpus they spent decades building.

We’ll keep it simple, visual, and practical—so you can have a real conversation with them when you go home next time.

The New Indian Retirement Reality

Thirty years ago, the standard retirement toolkit looked like this:

- Defined pensions for PSU and government employees

- Joint families, where parents lived with children

- Modest life expectancy and simpler lifestyles

Today’s retirement reality is very different:

- Fewer guaranteed pensions; more self‑funded retirement

- Smaller or nuclear families; children often in other cities or countries

- Longer life expectancy—20–30 years post‑retirement is common

- Higher medical inflation and lifestyle aspirations

A typical middle‑class retirement balance sheet today might look like:

- ₹60–80 lakh in EPF/NPS and mutual funds

- ₹20–40 lakh in FDs and small savings

- Owned home + maybe one rental property

- Children who can help—but who parents don’t want to depend on

That corpus now has to support 20–25 years of life.

So the real question isn’t just:

“Did they save enough?”

It’s:

“How does that pool of money turn into monthly income—without being killed by taxes or poor withdrawal decisions?”

And that’s where the mutual‑fund decision most retirees make on autopilot comes in:

IDCW (Income Distribution cum Capital Withdrawal) vs

SWP (Systematic Withdrawal Plan)

First, What Exactly Are IDCW and SWP?

Why “dividend” became IDCW

Until a few years ago, mutual funds offered a “Dividend” option. Many retirees thought:

“Dividend option = extra income on top of my investment, like company dividends.”

SEBI realised this was misleading. In 2021, it mandated that all such options be renamed IDCW – Income Distribution cum Capital Withdrawal.

Why?

Because what you get as IDCW is usually:

- A mix of your own capital + gains + dividends/interest the fund earned

- Paid out to you and then reflected as a drop in NAV

It’s not free extra money. It is, in economic terms, a withdrawal from your corpus.

IDCW vs SWP in one simple table

Here’s the core difference:

Put differently:

- IDCW = Fund pushes cash out, tax‑heavy, often poorly understood.

- SWP = You pull cash out, tax‑smarter, more controlled.

The Family Example: Same Corpus, Same Income Need

Let’s bring this down to a very believable example.

The setup

Your parents:

- Are both retired.

- Have ₹1 crore in financial assets they can use for retirement income.

- Of this:

- ₹60 lakh in equity mutual funds (growth option)

- ₹40 lakh in FDs as a safety buffer

- They also rent out one floor of their house.

Current inflows:

- Rent: say, ₹25,000/month (₹3,00,000 per year)

- FD interest: say, ~₹2,80,000 per year (assuming ~7% on ₹40 lakh)

Monthly expenses after retirement: roughly ₹80,000–90,000.

There’s a gap of ₹60,000/month (₹7,20,000 per year) that needs to come from the mutual fund corpus.

So, every year, ₹7,20,000 has to come out of that ₹60 lakh MF pot.

Now the key choice:

Should that ₹7,20,000 come through IDCW or SWP?

- Same family

- Same corpus

- Same withdrawal amount

But, as you’ll see, very different tax and behavioural outcomes.

How Tax Works: IDCW vs SWP (FY 2025–26 Rules)

Before we compare, a quick, simplified refresher on India’s current mutual‑fund tax rules.

IDCW taxation (all fund types)

- Whatever IDCW (formerly dividend) you receive from mutual funds is:

- Added to your total income, and

- Taxed at your slab rate (e.g., 5%, 20%, 30% + surcharge & cess).

- AMCs deduct 10% TDS if IDCW from that AMC exceeds ₹5,000 in a year.

So, for a retiree in the 30% slab, IDCW is effectively taxed at ~30% (plus cess), no indexation, no special benefit.

SWP taxation (equity funds)

When you run an SWP:

- Each instalment is a sale of some units.

- Only the gains portion (selling price – purchase price of those units) is taxed.

For equity‑oriented funds (current rules):

- Short‑term (≤12 months units held): gains taxed at a special STCG rate (about 20%)

- Long‑term (>12 months):

- Gains up to ₹1.25 lakh per year across all equity funds and stocks are tax‑free.

- Gains above that threshold taxed at 12.5% (approx.), without indexation.

Important: in most retirement SWP scenarios, the bulk of the monthly payout is actually your own capital, especially in the early years. The taxable gain portion is often much smaller than the total SWP amount.

Side‑by‑Side: Year 1 Tax Hit – IDCW vs SWP

Let’s compare Year 1 of retirement for our example family.

Assumptions (for illustration, not as advice)

- Parents fall effectively into the 30% tax slab once rent + FD interest + other income is added.

- Mutual funds are equity‑oriented and held for more than 1 year (so withdrawals are long‑term).

- Equity portfolio generates, say, 8–10% average annual return over time (this is only a working assumption).

Now look at how that ₹7,20,000 yearly withdrawal is treated:

Table 1: Year‑1 tax treatment

These numbers are just to give you an order of magnitude. The direction is what matters:

- Under IDCW, the full payout is dragged into the tax slab.

- Under SWP, only the profit portion (often a minority) faces capital‑gains tax, with an annual ₹1.25 lakh LTCG cushion on equity gains.

Over 10–15 years, the cumulative tax difference can easily run into several lakhs, even with the same corpus and same withdrawals—purely because one method is more tax‑efficient by design.

The Tax Bill That Quietly Grows Over Time

Year‑1 math is only half the story. Retirement is not a one‑year event; it’s a 20–25 year journey.

And in that journey, your parents’ income sources rarely stay flat.

How income typically evolves in retirement

Over the years, all of this tends to happen:

- Rent increases every 2–3 years (₹20,000 → ₹30,000 → ₹40,000 per month).

- Old FDs mature and get reinvested at higher amounts as the corpus grows.

- A property might eventually be sold, adding capital that generates interest.

- There may be some consulting or part‑time income in the early retirement years.

Each event feels small in isolation. Together, they slowly push total income up the tax ladder.

Now see what happens to our two options.

Under SWP (Growth + SWP route)

- The ₹7,20,000 SWP is still composed of:

- A big chunk of principal (not taxed)

- A gains portion, taxed as capital gains

- Even as rent and FD income grow, the SWP cash flow itself doesn’t get added to “income” for slab purposes—only the gains do.

- The ₹1.25 lakh per year LTCG exemption on equity gains remains available every year.

Result:

The tax drag on the MF withdrawal grows much more slowly.

Under IDCW

- The entire ₹7,20,000 IDCW is inside the taxable income pile from Day 1.

- When rent rises from, say, ₹3 lakh to ₹4 lakh to ₹5 lakh a year, and FD interest climbs, all of this stacks on top of the IDCW.

- Over time, retirees can get pushed into higher slabs or deeper within the same slab, purely because their “income pile” keeps getting taller.

Result:

The effective tax rate on each rupee of IDCW tends to creep upward over time—even if the withdrawal amount (₹7.2 lakh) never changes.

Behavioural Angle: Control vs Illusion of “Income”

Apart from tax, there’s a behavioural difference investors often ignore.

IDCW: Feels like “income”, but masks what’s happening

- Regular IDCW credits create the illusion of “income from the fund”.

- Many retirees don’t notice that NAV falls after each payout and that they’re effectively eating into their own capital.

- Because it looks like “the fund is paying me,” they may underestimate how fast their corpus is depleting, especially if the scheme’s performance is mediocre.

SWP: Makes withdrawals visible and deliberate

- Every SWP instalment is a visible redemption of units—you can see units sold, NAV, remaining balance.

- This makes it easier to:

- Track the pace of drawdown

- Adjust withdrawal amounts if markets have a very bad year

- Maintain a sense of ownership and control over the corpus

In retirement planning, clarity beats convenience. SWP may feel a little more “technical” at first, but it often leads to better awareness and more responsible decision‑making.

Quick Comparison Table: IDCW vs SWP for Retired Parents

| Dimension | IDCW (Payout Plan) | SWP (Growth + SWP) |

|---|---|---|

| Tax on ₹7.2L withdrawal | Entire ₹7.2L taxed at slab rate | Only gains portion taxed as capital gains; principal is tax‑free |

| Impact of rising rent/FD income | Pushes total income higher; more of IDCW taxed in higher effective slab | SWP gains still taxed as CG; rest of payout not in slab‑income pile |

| Control on timing/amount | Payout frequency/amount depends on scheme; may change or stop | You set withdrawal amount and date; fully customisable |

| NAV visibility | Many retirees ignore post‑IDCW NAV drop | Corpus and unit balance clearly visible as units are redeemed |

| Suitability | Rarely best for high‑tax‑bracket retirees relying on MF for income | Generally more tax‑efficient and transparent for planned retirement income |

The Real Retirement Questions to Ask Your Parents

Before your parents (or you) default to IDCW or SWP, here are the conversations worth having.

1. “How much do you really need each month?”

- Break down their actual monthly expenses—core and lifestyle.

- Identify which parts are covered by pensions, rent, FD interest.

- The gap is what needs to come from mutual funds / other investments.

2. “What’s your total expected taxable income already?”

- Add up rent, interest, any pension, part‑time work.

- See which tax slab they’re already in before touching mutual‑fund withdrawals.

- If they’re already close to or inside the 20–30% slabs, IDCW will be especially punitive.

3. “Are they OK adjusting withdrawals in bad market years?”

- IDCW feels fixed, but schemes can cut or skip payouts too.

- With SWP, you have more flexibility to temporarily reduce withdrawals in very bad markets to protect the corpus.

- Ask if they’re comfortable with the idea that income can be nudged up or down if needed.

4. “Who will help track tax and paperwork?”

- IDCW: shows up as dividend/IDCW income in AIS and Form 26AS; TDS may be cut.

- SWP: shows up as capital gains; you (or your CA) need to reconcile capital‑gains statements at filing time.

Make sure someone—you, a sibling, or a trusted adviser—is actually looking at these reports once a year and not just at the bank balance.

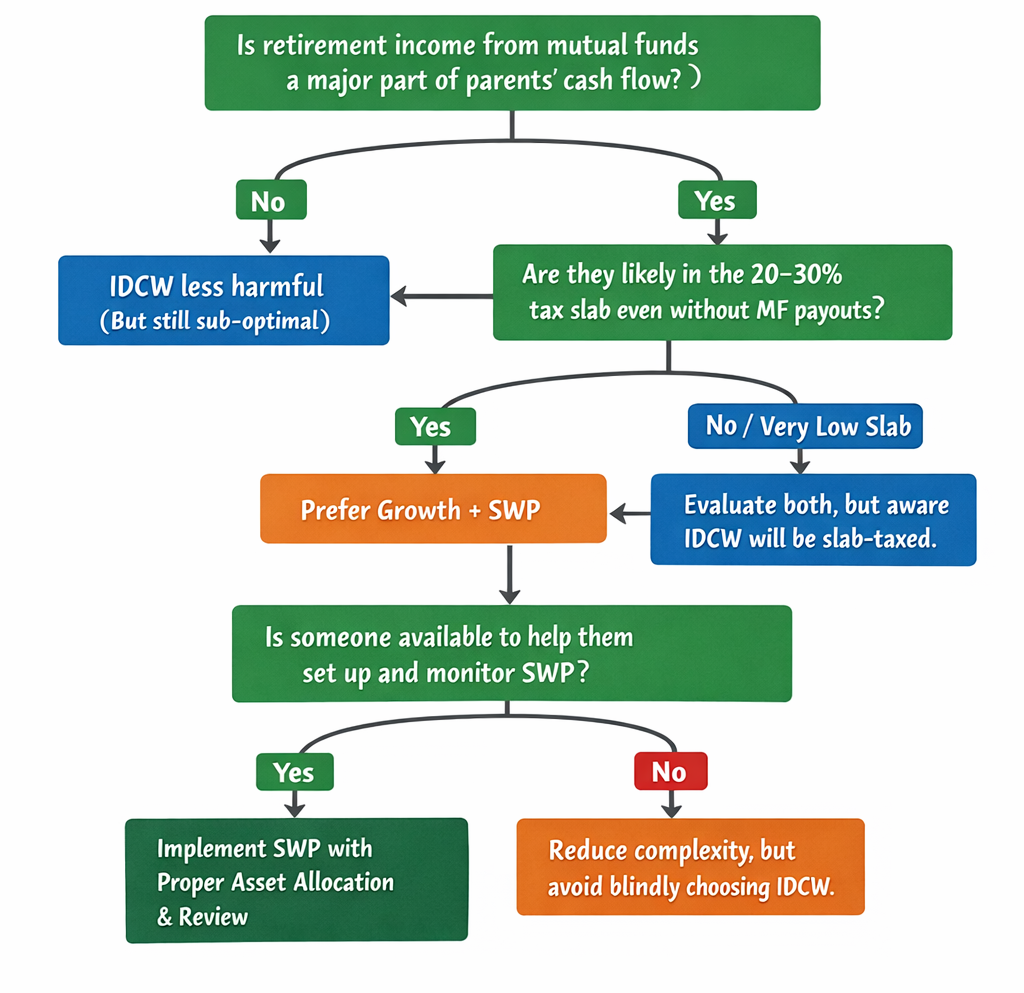

Decision Flowchart

How You Can Help—Without Taking Over

Parents can be sensitive about money. They’ve taken pride in “handling things” all their lives.

The goal is not to barge in and say, “You did it all wrong.” It’s to:

- Respect what they’ve already built

- Bring in the new tax and product understanding you have access to

- Make a few key decisions smarter—so their money lasts longer

A simple script:

“Papa/Maa, I was reading about how mutual fund payouts are taxed nowadays. Earlier ‘dividends’ are now called IDCW and they’re fully added to income.

For someone in your tax bracket, there’s another option called SWP where only the profit part is taxed, and often at a lower rate. Over 15–20 years, the difference can be several lakhs.

Can we sit with your adviser or CA once and just check whether changing the plan makes sense? We don’t have to decide today—I’d just feel better if we had looked at it together.”

You’re not questioning their choices. You’re upgrading the withdrawal plumbing for a world that changed under their feet.

Key Takeaways

- For today’s Indian retirees, the challenge is not just how much they saved, but how they draw it down.

- IDCW (old dividend option) is:

- Taxed at slab rate on the full payout

- A mix of capital + income, often misunderstood

- Likely to push total taxable income higher as rent and interest rise

- SWP from a growth plan is:

- Taxed only on the gains portion of each instalment, often at favourable capital‑gains rates

- More transparent and controllable

- Typically more tax‑efficient over a 15–25‑year retirement horizon

- Over long retirements, the difference between IDCW and SWP can easily add up to lakhs in extra tax, without any change in the underlying funds.

- The most important retirement conversation with your parents may have nothing to do with which mutual fund they picked—but how the money comes out.

If you can help them get that part right, you’ve already done more than most.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment, financial, tax, or legal advice. The explanations of IDCW and SWP, tax treatments, and example scenarios are based on the mutual fund taxation framework in India for FY 2024–25 and FY 2025–26 as summarised by public sources such as SEBI circulars, AMFI/AMC disclosures, and independent tax guides.

Tax rates, exemption thresholds, and rules (especially for capital gains and IDCW) are subject to change by future Finance Acts, and actual tax liability depends on an individual’s total income, chosen tax regime, residential status, and other factors. The family and numerical examples in this article are illustrative, simplified, and not projections or guarantees of outcomes.

Investing in mutual funds involves market risk, including possible loss of principal. Past performance and historical tax rules are not indicative of future results. Before making decisions about IDCW vs SWP, retirement income strategies, or any investment product, you should carefully evaluate your own or your parents’ financial situation, goals, and risk tolerance, and consult a SEBI‑registered investment adviser, qualified tax professional, or chartered accountant.