Last year at a family get-together, Suman, a 32-year-old marketing professional, found herself in a familiar conversation.

Her cousin had just bought a flat in Pune. He was excited, but also worried. The down payment had wiped out most of his savings. The EMI felt heavy. The society had already announced a repair fund. Rent would come in eventually, but for now, the property was more stress than cash flow.

Suman, on the other hand, had a very different story. She had just put ₹1 lakh into Embassy REIT, which owns Grade-A office parks in cities like Bengaluru, Mumbai and Pune. Every quarter she received distributions in her bank account, without dealing with tenants, brokers or leaky bathrooms.

In her words:

“I own commercial properties in India’s hottest markets, and I did not even have to move furniture.”

Suman is not an exception. Quietly, a lot of Indians are discovering REITs as a way to participate in real estate without the huge cheques and headaches that come with buying a flat.

This article is about that shift. What REITs are, how they work in India, what the returns and taxes look like, and how you can decide if they fit into your portfolio.

What Exactly Are REITs?

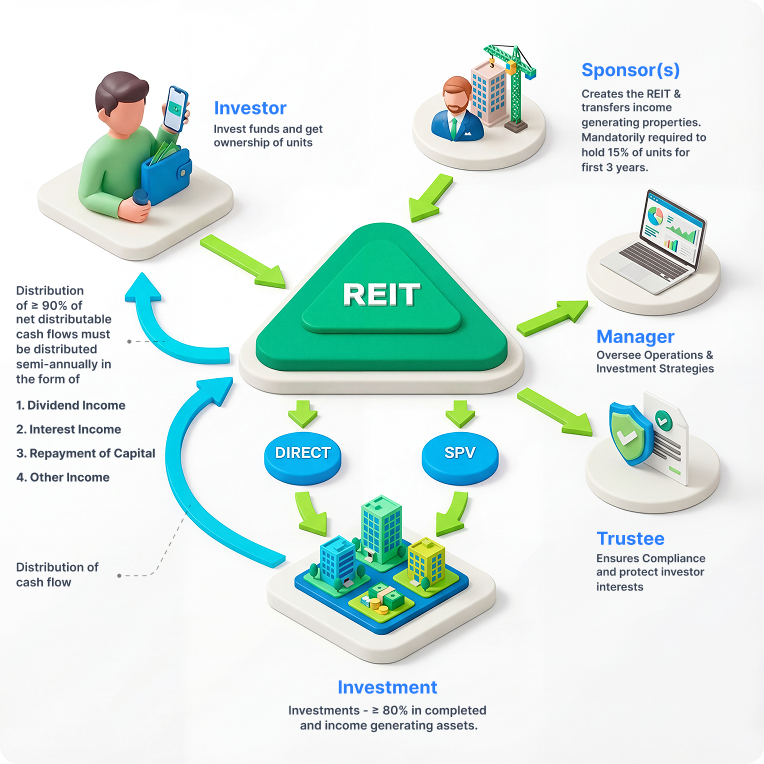

REITs (Real Estate Investment Trusts) are SEBI-regulated business trusts that own and operate income-generating real estate.

Typical assets include:

- Office parks and IT campuses

- Shopping malls and high-street retail

- Warehouses and logistics parks

- Hotels and other commercial properties

Instead of buying a whole building, you:

- Buy units of a REIT on the stock exchange, like you would buy shares.

- The REIT owns the properties through special purpose vehicles (SPVs), collects rent and other income, pays expenses and interest, and then pays out most of the remaining cash to unitholders.

SEBI rules require that:

- At least 80 percent of a REIT’s assets must be in completed, income-generating properties.

- At least 90 percent of net distributable cash flow must be distributed to unitholders, usually every quarter or half-year.

So REITs are essentially:

A pool of high-quality commercial properties that you can access in small ticket sizes, with regular payouts and stock-like liquidity.

India’s REIT Moment

India was late to the REIT party, but things are picking up.

- Embassy Office Parks REIT listed in 2019 as India’s first REIT and is now one of Asia’s largest by area.

- As of early 2026, there are five listed REITs: Embassy REIT, Mindspace REIT, Brookfield India REIT, Nexus Select Trust and Knowledge REIT.

- SEBI has reduced the minimum investment from ₹50,000 earlier to about ₹10,000–₹15,000, and cut the minimum lot size from 100 units to 1 unit to make REITs truly retail-friendly.

In practice:

- You can buy even one unit of a listed REIT on NSE or BSE.

- Unit prices often trade in the ₹350–₹600 range, so a starting ticket can be just a few hundred or a few thousand rupees.

That is a far cry from the ₹20–50 lakh cheque most people associate with real estate.

How REITs Actually Make Money For You

At a high level, REIT returns have two parts:

- Cash distributions

- Come from rental income, interest and other cash flows.

- Often work out to 4–7 percent annually as a yield at current prices, depending on the REIT.

- Capital appreciation

- As rents grow over time and properties get revalued, unit prices can rise.

- Over long periods, total returns can be competitive with other income assets.

Take Embassy REIT as an example:

- It owns around 51 million sq ft of commercial assets across Bengaluru, Mumbai, Pune, Chennai and NCR, with roughly 40.9 msf completed and about 90 percent occupied.

- Since listing in 2019, it has distributed over ₹13,800 crore to unitholders, with a very high payout ratio over 27 consecutive quarters.

- Over the last five years, its total return profile (price plus distributions) has been in the low to mid-teens annualised, depending on the entry point and reinvestment of payouts.

Those numbers will move around with markets, but they show that:

REITs are designed to behave more like a steady income plus moderate growth product, rather than a 20 percent plus high risk equity stock.

Suman’s Example: What Can ₹1 Lakh In A REIT Do?

Let us go back to Suman’s story.

Assume she invested ₹1 lakh in Embassy REIT on 1 April 2021 and held it for five years. Based on the sort of yields and price performance we have seen in recent years, a reasonable illustration could look like this:

- Total value after 5 years: about ₹1.6 lakh

- Implied total return: roughly 11.5–12 percent per year, including:

- Around ₹33,000 received as cash distributions into her bank account over five years

- Around ₹26,000 as net price appreciation on the units held

These are illustrative round numbers, not exact back-tested figures. They simply reflect the idea that:

- You get regular income, much like rent.

- You also participate in the growth of underlying property values and rentals.

The important part is not whether it is 11.2 or 11.8 percent in a given window, but that:

- Returns are meaningfully higher than a savings account or many bank FDs over similar periods,

- Without the operational burden of managing a physical property.

REITs vs Buying A Flat: A Simple Comparison

Here is a side by side look at what Suman did versus what her cousin did.

Table: REIT investment vs buying a residential flat

| Factor | REIT (like Embassy) | Buying a flat directly |

|---|---|---|

| Minimum ticket size | A few thousand rupees, even 1 unit | Typically ₹20–50 lakh plus for metros |

| Diversification | Dozens of properties and hundreds of tenants | One property, one location, maybe one tenant |

| Income stream | Regular distributions from rent-like cash flows | Rent, often intermittent or delayed |

| Management | Professional team, no day to day involvement | You handle tenants, maintenance, brokers |

| Liquidity | Can sell units any trading day on exchange | Selling a flat can take months |

| Transaction costs | Brokerage plus small STT and charges | Stamp duty, registration, legal, brokerage |

| Leverage | No EMI burden unless you borrow separately | Long term EMIs and interest outgo |

| Volatility | Market-linked unit price | Local property cycle and rental market risk |

This does not mean one is always better than the other. A home you live in is more than a spreadsheet. But if your goal is financial exposure to real estate as an asset class, REITs are a very compelling tool.

How REIT Income Is Taxed

This is where many people get confused, so let us simplify.

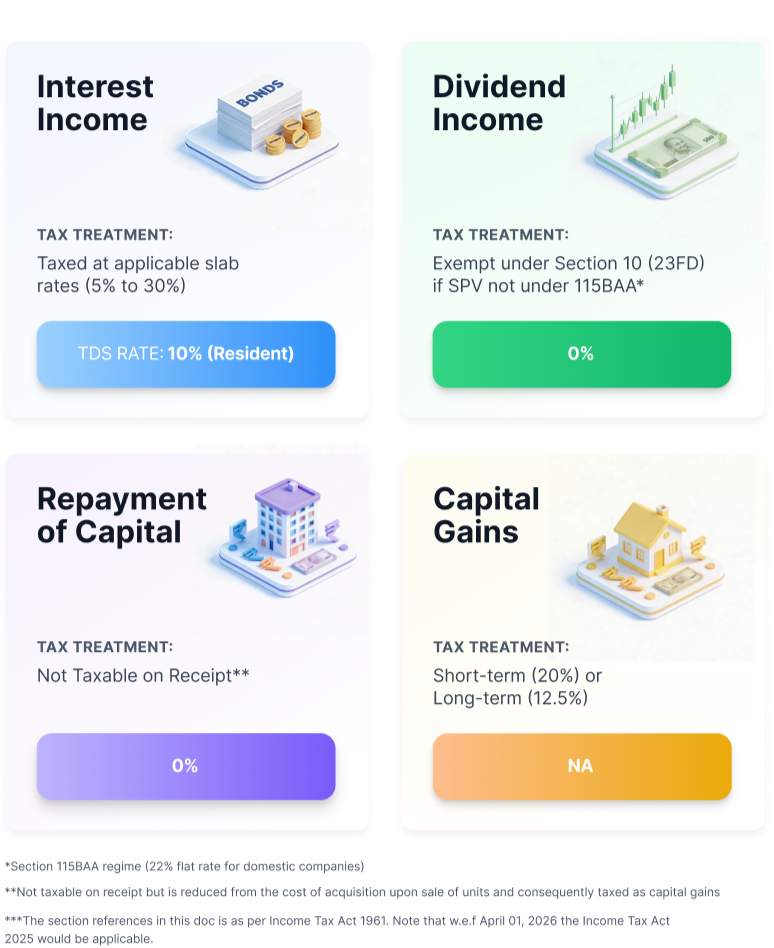

REITs in India enjoy a “pass-through” tax status under Section 115UA of the Income Tax Act.

The basic idea:

Income is mostly taxed in the hands of the unit holder, not at the REIT level, and it retains its character when it flows through.

If the REIT receives:

- Rent from tenants through its SPVs

- Interest from SPV debt

- Dividends from SPVs

then, when it distributes these to you:

- Rent-like and interest-like portions are taxed as “Income from Other Sources” at your normal slab rate.

- Dividend portions are treated as dividend income, again typically at slab rate under the current rules, depending on whether underlying SPVs have already paid DDT or other taxes.

When you sell your REIT units:

- If held up to 12 months, gains are short term capital gains, generally taxed at 20 percent for listed REIT units as per current guidance.

- If held more than 12 months, gains are long term capital gains, taxed at 12.5 percent with an exemption of up to ₹1.25 lakh of gains per year, without indexation for listed REITs.

There have also been recent changes where some parts of distributions that were earlier classified as debt repayment are now treated as taxable in the hands of unitholders, subject to cost of acquisition adjustments.

In short:

- REIT income is not tax free, but it is reasonably efficient, and you avoid double taxation at both trust and investor level on most streams due to the pass-through design.

Always check the latest tax rules or speak with a CA, because the exact mix of components in your distribution (interest, rent, dividend, principal repayment) matters for how much you actually pay.

How Easy Is It To Invest In REITs?

Practically, investing in a listed REIT is similar to buying any stock:

- Open a demat and trading account.

- Search for the REIT ticker, for example:

- Embassy Office Parks REIT (EMBASSY)

- Mindspace Business Parks REIT

- Brookfield India Real Estate Trust

- Nexus Select Trust

- Place a buy order for any number of units, even one.

SEBI’s move to reduce minimum investment and lot size has made this very accessible.

You can also:

- Systematically invest over time, just like an SIP, if your broker allows periodic orders.

- Hold REITs inside your overall asset allocation as part of the debt or alternative bucket, depending on how you classify them.

What Are The Risks You Should Be Aware Of?

REITs are not risk free. Before you copy Suman, it is important to know what can go wrong.

1. Interest rate and yield risk

REITs behave somewhat like high-yield, long-duration assets:

- If interest rates rise, market-required yields may rise, which can pressure REIT prices in the short to medium term.

- Conversely, falling rates can support higher valuations.

2. Vacancy and rental risk

If:

- Large tenants vacate,

- Entire micro markets slow down, or

- Work-from-home structurally reduces office demand in certain locations,

then the REIT’s:

- Occupancy levels,

- Rent renegotiations, and

- Future growth

can all be affected.

This is why looking at:

- Portfolio quality,

- City mix,

- Tenant profile, and

- Lease tenors

matters as much as the yield number.

3. Regulatory and tax changes

As we saw with the change in taxation of debt repayment distributions, the government can tweak tax treatment over time.

Future changes may:

- Make some components more or less tax friendly,

- Affect net post-tax yields.

4. Market price volatility

Although underlying properties move slowly, REIT units trade on exchanges. Their prices can:

- Swing with broader market sentiment,

- React to headlines about offices, IT sector, global rates, and risk appetite.

If you are going to panic every time the unit price dips 10 percent on sentiment, REITs may not be the right instrument.

Who Are REITs Best Suited For?

REITs tend to work well for:

- Salaried professionals who want real estate exposure without locking 80 percent of their net worth in a flat.

- Retirees or near-retirees looking for relatively stable cash flows with some inflation kicker, as part of a diversified income portfolio.

- Young investors building a core portfolio of equity, debt and one or two REITs for diversification.

- Anyone who likes the idea of “rent-like income without tenant drama.”

They may be less suitable for:

- Very conservative investors who want absolute capital stability like a bank FD.

- Traders who crave fast price moves and are not interested in income.

- People who already have a lot of their net worth tied up in property and may need more diversification in other asset classes.

How To Decide Between A Flat And A REIT For Investment

If your primary goal is a home to live in, that is an emotional and lifestyle choice. You can still own a home and invest in REITs on top.

If your primary goal is investment return, ask:

- What percentage of my net worth am I comfortable putting into a single, illiquid property?

- How will EMIs affect my cash flow, career flexibility and stress?

- Would I be better off with a mix of equity, debt and REITs, and maybe a smaller or later home purchase?

For many in Suman’s position, the answer is:

“I would rather build a strong financial base with diversified assets first, and then think about buying property on my own terms.”

REITs are a powerful tool in that plan.

Final Thoughts: Why REITs Are Changing How Indians Think About Property

For decades, the default script was simple:

- Study, get a job,

- Save for down payment,

- Buy a flat,

- Pay EMIs for 20 years.

Today, that script is being rewritten.

With REITs:

- You can start participating in commercial real estate with very small amounts.

- You get regular income, professional management and easy exits.

- You are no longer forced to choose between “all-in on one property” or “no real estate at all.”

That does not mean you should throw all your money into REITs. They are one tool among many. But if you have been postponing investing in property because the numbers did not add up, it may be worth doing what Suman did.

Start small. Understand the product. Fit it into a sensible asset-allocation plan. Then let time and discipline do their work.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment, tax, legal or other professional advice. References to specific REITs such as Embassy Office Parks REIT, Mindspace REIT, Brookfield India REIT and Nexus Select Trust are for illustration and educational context only and do not represent recommendations to buy, sell or hold any security.

Regulatory details about REIT asset allocation and distribution requirements are based on SEBI regulations and related commentary, including the requirement that at least 80 percent of REIT assets be invested in completed, income-generating properties and that at least 90 percent of net distributable cash flows be distributed to unit holders. Tax explanations draw on Section 115UA and related provisions governing pass-through treatment and the taxation of REIT income and capital gains in the hands of investors. Actual tax treatment depends on your individual situation and may change with future amendments.

Any return figures, yields or growth examples (including the ₹1 lakh Embassy REIT illustration) are indicative and simplified, based on historical patterns and public data, and are not guaranteed or predictive of future performance. REIT prices and distributions can fluctuate, and investors may lose money. Before making any investment decision, especially in REITs or other market-linked products, you should carefully evaluate your financial situation, risk tolerance and investment objectives, and consult a SEBI-registered investment adviser or qualified professional.