🌍 Introduction: When a Tax Cut Became a Turning Point

When India’s GST Council announced a complete exemption of GST on individual health and life insurance premiums in September 2025, most headlines were short and technical.

But within weeks, something unexpected happened. Insurance offices were flooded, online policy sales soared, and the long-ignored health cover segment turned into India’s newest financial frenzy.

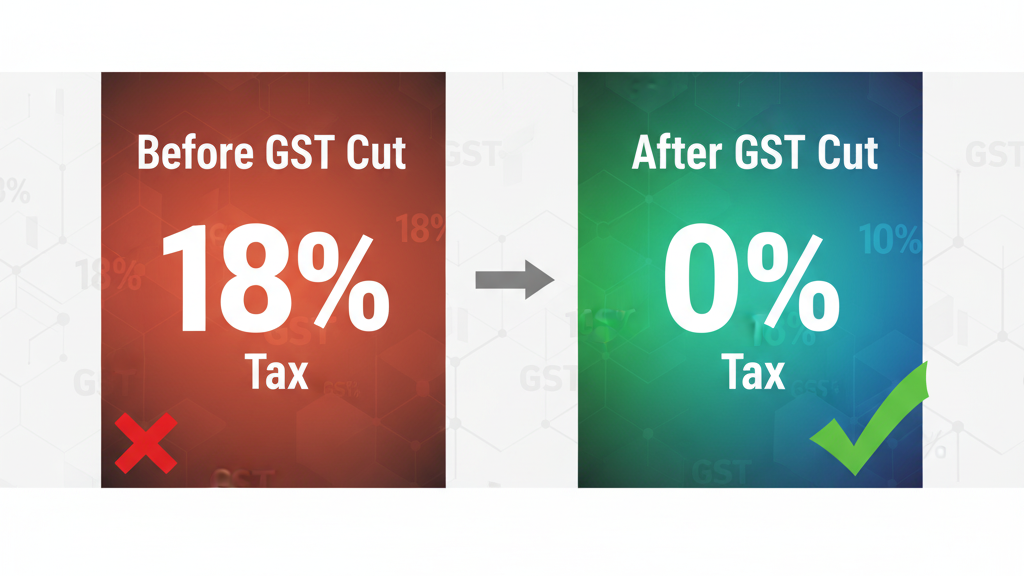

The 18% GST that once inflated premiums vanished overnight, and with it disappeared one of the biggest psychological and economic barriers to buying insurance.

💡 The Policy That Changed the Game

On 22 September 2025, the GST Council made a landmark decision:

Individual life and health insurance policies would no longer attract GST.

Before this reform, insurers added 18% GST to every premium. For example:

- Rs. 25,000 annual premium → Rs. 29,500 with GST

- Rs. 50,000 annual premium → Rs. 59,000 with GST

For a middle-class family with multiple policies, that difference wasn’t minor, it was decisive.

Now, the same Rs. 50,000 policy costs Rs. 50,000.

That 18% drop translated into immediate affordability. And when combined with rising healthcare costs, pandemic-era health consciousness, and digital access, it was a spark in a field of dry grass.

📈 The Boom in Numbers

The results were fast and unmistakable:

- Standalone health insurers (SAHIs) recorded a 38.3% YoY jump in premiums in October 2025, Rs. 3,738 crore vs Rs. 2,703 crore a year earlier.

- The overall health insurance industry (including general insurers) grew 7.7% in H1 FY26 to Rs. 64,240 crore.

- Online policy sales spiked sharply: Insurance aggregators reported record traffic and conversions within 10 days of the announcement.

- Google searches for “best health insurance plan India” rose 65% week-on-week in early October 2025.

The surge was broad-based. Urban, semi-urban, and even rural households showed renewed interest in buying or upgrading coverage.

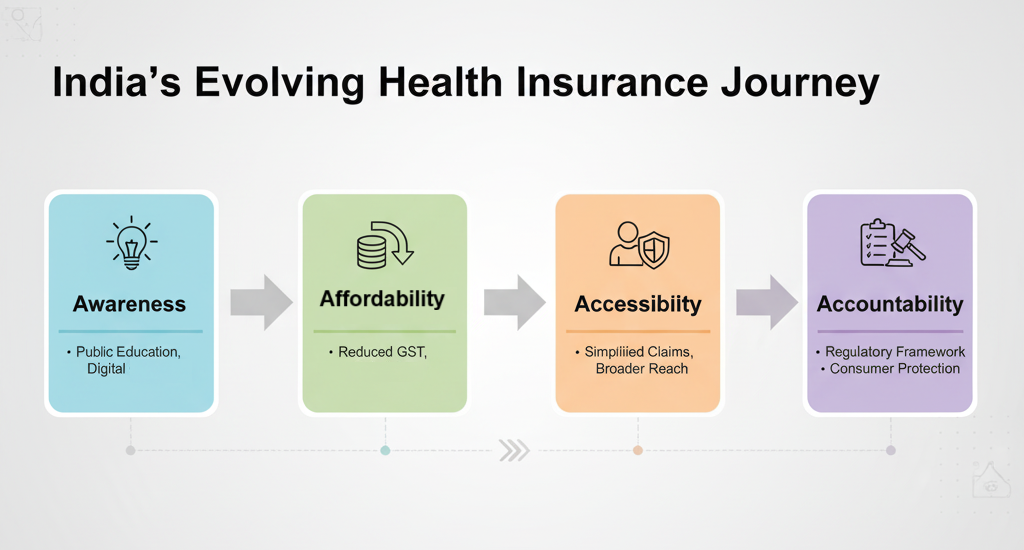

🧮 Why the GST Cut Worked

1️⃣ Affordability Meets Awareness

For years, affordability was the biggest reason many Indians stayed uninsured. The pandemic changed that, people understood why they needed health cover. The GST cut addressed the how.

2️⃣ Middle-Class Catalyst

The biggest surge came from India’s growing middle class. Salaried professionals, small business owners, and gig workers who were price-sensitive but willing to spend if convinced of value.

3️⃣ Digital Distribution

Platforms like PolicyBazaar, Coverfox, and BankBazaar turned the tax change into marketing gold:

“Now that GST is gone, so are excuses to stay uninsured.”

Within weeks, digital platforms reported 2–3× sales growth.

4️⃣ Insurer Push and Product Innovation

Insurers seized the moment to repackage products, offering higher coverage (Rs. 10–Rs. 20 lakh) for family floaters and senior citizens. Many even bundled wellness perks and OPD benefits.

🧭 The Real Winners : Consumers

🩺 First-Time Buyers Flood the Market

For millions, this was their first entry into health insurance. Removing GST made policies seem not just cheaper but fairer, especially since medical inflation was rising faster than wages.

🧓 Senior Citizens Finally Buying

The elderly, often deterred by high premiums, became an important segment post-cut. Insurers reported increased demand for senior-citizen and critical-illness plans.

👨👩👧 Families Upgrading Cover

Households already insured used the opportunity to double their coverage or add dependents, often using their “GST savings” to justify it.

Compare: Top Family Floater Health Plans in India for 2025

💬 What Insurers and Experts Are Saying

✳️ “It’s like Diwali for Health Insurers.”

A senior executive at Star Health Insurance told The Times of India that October 2025 was their best sales month in three years. (Source)

✳️ Policybazaar CEO Yashish Dahiya said:

“The GST relief didn’t just make insurance cheaper, it made it emotionally easier to buy.”

✳️ IRDAI’s Perspective:

Regulators see this as a way to raise retail penetration, which remains low at under 4% of the population.

⚖️ The Caveat : Who Really Gains?

Not everyone is celebrating without reservations.

❗ Loss of Input Tax Credit (ITC)

When GST goes to zero, insurers can no longer claim credit for taxes paid on services (marketing, reinsurance, admin). That loss could lead to a 3–5% rise in base premiums to offset the impact. (Financial Express)

In short, the sticker price is down, but the hidden cost might creep up again.

❗ Uneven Pass-Through

Not all insurers have passed the full benefit to consumers. Some have used the cut to shore up margins or offset prior claim inflation. Transparency remains patchy.

❗ Agent Margin & Distribution Strain

Agents’ associations argue that removal of ITC makes their operations more expensive. The Insurance Agents Welfare Association (IAWA) even staged protests, calling it “a reform with pain built in.” (India Today)

🏦 Section 7: Economic Ripples : Beyond Insurance

The GST exemption doesn’t just affect insurers, it affects the broader economy.

📊 Rising Household Financialization

The tax relief nudged millions toward formal financial products. Alongside mutual funds and SIPs, health insurance became part of the “responsible portfolio.”

🧭 Boost to Domestic Health Ecosystem

Hospitals, TPA networks, and diagnostic partners benefit from higher coverage rates, better pay-outs, more planned hospitalizations, and predictable revenue.

💼 Employment & Distribution

With insurance demand surging, insurers and brokers are hiring aggressively, from call-center reps to field agents.

🔍 Risks That Could Derail the Party

- Medical Inflation:

Hospital and diagnostic costs are rising at 12–14% annually, faster than income growth. Without strong underwriting, premiums could rebound upward. - Policy Complexity:

New entrants may buy low-cost plans without understanding exclusions, sub-limits, or co-pays. - Short-Term Sales Focus:

Insurers may chase volume without ensuring claims efficiency, risking consumer backlash. - Regulatory Overcorrection:

If insurers raise prices to recover ITC, public sentiment could turn, triggering policy reversals.

🩹 The Long-Term Impact : More Coverage, Smarter Consumers

If sustained, the GST cut could permanently alter India’s insurance culture:

- From optional to essential: Health cover becomes as normal as mobile or Wi-Fi bills.

- From metro to Bharat: Rural and semi-urban adoption accelerates through PMJAY and private tie-ups.

- From reactive to preventive: Insurers are adding wellness incentives, gym reimbursements, and health-tracking apps.

- From annual to lifelong cover: Younger Indians are buying early, making lifetime coverage more affordable.

📘 What You Should Do Now

✅ If You Don’t Have a Policy Yet

Buy one now, while premiums are low and insurers are competing for customers. Choose comprehensive coverage, not just cheap plans.

✅ If You Already Have a Policy

Renew under the zero-GST regime. Use this as a trigger to:

- Increase sum insured

- Add family members

- Review hospital networks

✅ If You’re a Senior Citizen

The tax cut has made high-value policies slightly easier to afford. Look for plans with no room rent cap and lifetime renewability.

Guide: Best Health Insurance Plans for Senior Citizens 2025

📊 Future Forecast — What Comes Next

| Trend | Projection (2026–2030) | Implication |

|---|---|---|

| Retail Health Premium Growth | 18–20% CAGR | Expanding individual coverage base |

| Average Sum Insured | From Rs. 6 L to Rs. 12 L | Upgrading middle-class protection |

| Rural Market Share | From 18% → 32% | Rising penetration |

| Claim Ratios | 88–95% range | Pressure on underwriting margins |

| Policy Renewals | 90% retention | Strong long-term customer base |

💬 Voices from the Ground

“For once, a government reform feels like it reached people like me. I finally bought my first health plan.”

— Reena S., Teacher, Nagpur

“I didn’t realize how much GST was adding until I renewed this year. I used the savings to add maternity cover.”

— Ashok V., 34, Bengaluru

“Earlier, I thought insurance was a luxury. Now, it’s survival.”

— Manoj K., Taxi driver, Jaipur

🧩 Conclusion : Beyond the Tax, Toward Trust

The GST cut on health insurance may go down as one of India’s most quietly powerful financial reforms.

By lowering costs, it opened doors. By sparking demand, it drew insurers deeper into everyday lives. But the real victory isn’t in policy numbers; it’s in perception.

For decades, health insurance felt optional. Now, it feels essential.

Yet this moment needs stewardship. Transparency, fairness, and continued education, so that affordability leads not to complacency but to better protection.

If the industry can balance growth with accountability, India’s “zero GST” era may one day be remembered as the moment when health insurance finally became a habit, not a hesitation.

Further Reading

- Health insurance penetration in India

- Medical inflation and healthcare costs

- Tax-free investments and insurance

- Digital insurance platforms

- Insurance claim ratios explained

- Health cover for senior citizens

- Term vs Health Insurance